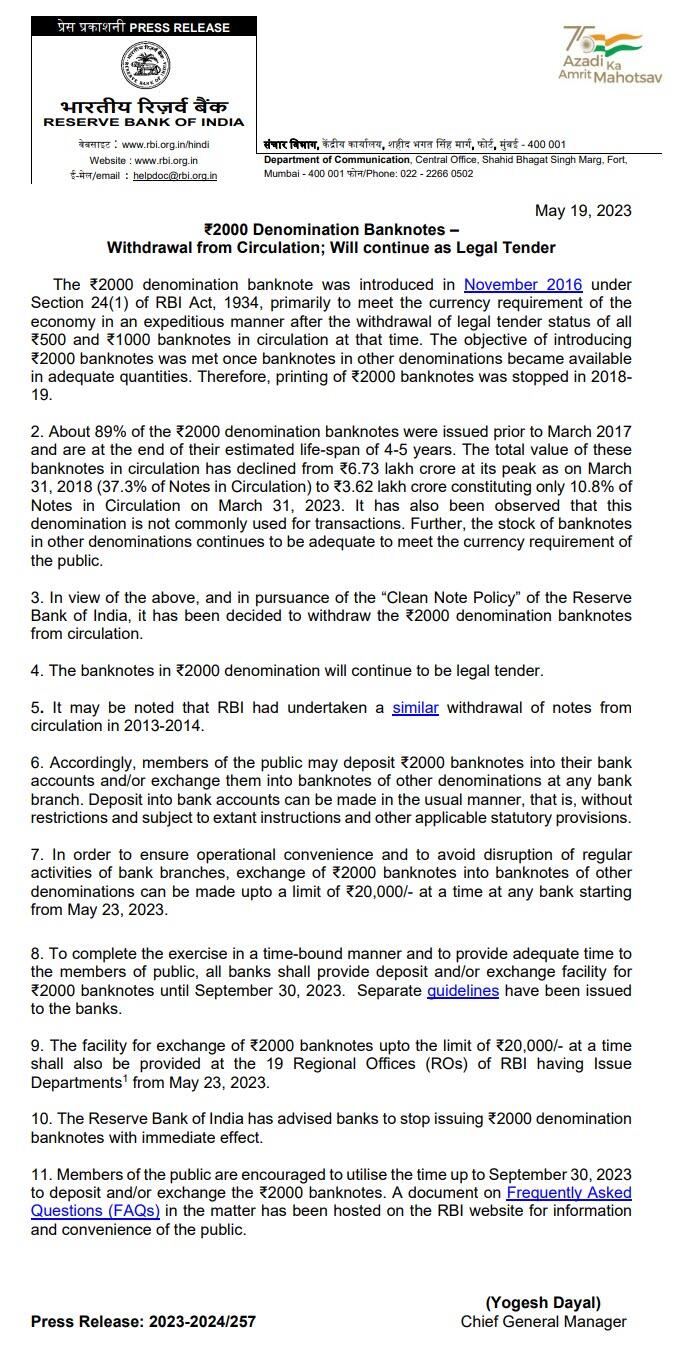

HK dollar de-peg argument gains new currency

William Pesek

As China angles to increase the yuan’s role in trade and finance, economists are wondering what it means for Hong Kong’s long-time peg to the US dollar.

The will-the-peg-survive question has popped with regular popularity since the late 1990s amidst the Asian financial crisis. One such episode was in November last year when New York hedge fund manager Bill Ackman announced he was betting against the peg.

At the time, Ackman’s Pershing Square Capital Management cited Sino-US decoupling tensions as a rationale. That, he seemed to believe, raised the odds Hong Kong might be forced to end the peg.

And that the turmoil would make the trade profitable, unlike previous attempts by Hayman Capital’s Kyle Bass and

George Soros decades before that.

Enter economist Andy Xie, who last week argued it’s time to ditch the US peg and link the Hong Kong dollar to the yuan. It’s hardly a new idea, but one Xie, a former top Morgan Stanley economist, argues has come of age in a recent South China Morning Post op-ed.

The gist of his argument is that “Hong Kong’s currency peg to the dollar is not sustainable. The city risks being increasingly led by US monetary policy as the utility of the fully convertible Hong Kong currency in meeting China’s demand for US dollars is fading. As global yuan demand grows, switching to that currency would boost Hong Kong’s financial fortunes.”

How likely is this? Not very, at least for the foreseeable future. Neither Chinese President Xi Jinping nor new Premier Li Qiang appears ready to make such a momentous change to a 40-year policy that’s served the greater China region quite well.

To be sure, the peg is now generating serious economic headwinds, warranting brainstorming in Beijing. US inflation at near 40-year highs and aggressive

Federal Reserve tightening are forcing Hong Kong to tweak monetary policies in kind, undermining the business hub’s growth potential.

As Xie puts it: “With China’s interest rates expected to stay lower than US rates, due to lower Chinese inflation, embracing the yuan would stabilize Hong Kong’s asset markets. Sticking with a US-pegged currency, however, means exposure to volatility.”

Xie adds that “entrenched US inflation threatens to bring back dollar swings like in the 1970s and/or US interest rate surges like in the 1980s — the effect on Hong Kong could devastate its property market.”

Again, President Xi’s financial team hasn’t displayed much tolerance for risky policy shifts. But to economist Raymond Yeung at ANZ Bank, Xi’s ambitions for the yuan — including putting it at the center of oil purchases — are forcing the Hong Kong dollar’s peg back into the global spotlight.

“As geopolitics and economies change, so do pressures on the HK dollar peg,” Yeung says. “In recent months, more countries have expressed interest in using the yuan for transactions with China.”

What’s more, he notes, “the potential emergence of a ‘

petro-yuan’ regime may seem to promote the reserve currency status of the Chinese yuan. Speculation about pegging HK dollars with the renminbi and ending the US dollar’s hegemony is also intensifying.”

China’s yuan is gaining ground as a currency of trade. Image: Twitter

That intensity can be found in surging interbank rates in Hong Kong. It reflects a drop in banking system cash amid speculation of tighter monetary conditions to come. In mid-May, the Hong Kong Interbank Offered Rate rose to its highest level since December 2019.

The need for the Hong Kong Monetary Authority to keep the city’s currency in a tight range of 7.75 to 7.85 to the US dollar is complicating financial management. Over the last month, the HKMA’s aggregate balance – a key barometer of the amount of cash in the system – hit HK$44.5 billion (US$5.7 billion).

That’s the lowest since the 2008 global financial crisis. More recently, on May 30, Hong Kong’s de facto central bank loaned nearly US$500 million through its discount window.

The main cause for such liquidity squeezes is that “the Fed’s rate hike in June is on the table,” notes strategist Ken Cheung at Mizuho Bank.

Strategist Cheung Chun Him at Bank of America notes that

HKMA might have to serve more and more as “lender-of-last resort” as the “scramble for funding will be particularly acute” through the end of the current quarter.

That’s becoming harder, though, as US Federal Reserve rates and those being set by the People’s Bank of China diverge.

Many economists make the argument that in order for the yuan to become a reserve currency rival to the US dollar, China’s financial system would benefit from more explicit ties to Hong Kong’s. This dynamic, though, works both ways.

“Since the city is highly integrated with China’s economy, the currency should be compatible with China’s business cycle instead of that of the US,” says ANZ Bank’s Yeung.

As peg speculation rises, Yeung thinks it’s useful to view things through the lens of Nobel laureate

Robert Mundell’s 1960s theory of the “optimal currency area.” Mundell’s framework, Yeung notes, “seems to lend support because using the same currency for economies in a single market should promote economic efficiency.”

To be sure, Yeung hedges, “it’s not totally applicable to Hong Kong because the renminbi market has been extended to it. Trade, investments and financial flows can already be transacted in Chinese yuan.”

But “in our view, the yuan could eventually be a functioning currency in the stock market for transactions, including dividend payments, amid increased acceptance by global investors. Therefore, there is no need to impose unnecessary changes on the existing peg.”

Yeung speaks for many when he argues that “unnecessary change may do more harm than good.” He adds that “in short, stability is key. Although there have been rising concerns about the long-term outlook of the US dollar after the recent banking crisis, it remains a global standard.”

Looking forward, Yeung notes, China’s Belt and Road Initiative “may also attract new segments of investor interest. Countries worried about ‘

weaponization’ of the US dollar could also see an alternative in the HK dollar as Hong Kong maintains free capital flows and its legal system is based on the common law.”

Still, speculators like Ackman think the Hong Kong peg’s days are numbered. The city’s precarious place is between a US that’s ratcheting rates higher and a China moving in the opposite direction. Some economists worry China is hurtling toward deflation, exacerbating Hong Kong’s troubles.

As Hong Kong struggles to straddle these two giants, it’s shackled with exactly the wrong monetary policy at a challenging moment. The straight jacket Hong Kong is forced to impose on itself could exacerbate the economic strains already damaging the government’s legitimacy, not least due to some of the worst income inequality in the

developed world.

The tensions emanating from the currency peg have only grown over the last five years, in part because of Chinese money bidding up already elevated property prices. As economist Vincent Tsui at Gavekal Research points out, home prices have increased by double digits year after year.

“But if we look at the household income growth,” Tsui notes, “that has been stalled since 2018, before the social unrest, before the pandemic.”

“So basically, this dividend from the economic integration with China has been exhausted. Second, it’s the debt servicing costs, right. So there has been a period of extra low interest rate for a decade. And now actually the interbank rates are triple the level we have seen over the past decade,” says Tsui.

“So, two factors combined together on the demand side, have pretty much weakened as well. The whole supply-demand dynamic is switching in the Hong Kong housing market, making it a much shakier ground as we have seen before,” he adds.

Such risks might reduce the tolerance for fundamental changes to the mechanics of

Hong Kong’s financial system. No piece is more central than the US dollar peg – or more destabilizing if a change were announced.

Ackman’s case against the Hong Kong peg has its merits, just as Bass’s did before Hayman Capital closed out its short position in 2021. This goes, too, for Soros in the late 1990s. And Xie’s take also makes some great new points.

Economist Andy Xie has raised fresh doubts about the Hong Kong dollar’s peg. Photo: Screengrab / BBC

“Riding on the yuan’s rise would be a big plus for Hong Kong,” Xie explains. “The yuan accounts for just over 2% of the

global payments system, and about the same in global forex reserves. China accounts for about 18% of the world economy and around 30% of global manufacturing output.

“The yuan’s share in global payments and currency reserves is bound to rise. Before it becomes fully convertible, Hong Kong has a unique opportunity to ride its rise and consolidate its status as a global financial center,” he says.

The first step, Xie adds, could be Hong Kong “starting the transition” by shifting the government payroll to yuan and collecting taxes in yuan. “As the

stock market gradually makes the shift, along with asset markets and the real economy, bank deposits and credit would follow naturally,” Xie argues. “The

Hong Kong dollar would fade away.”

Yet for any of this to happen, Xi’s government would have to display a level of audacity and risk tolerance it hasn’t over the last decade, economists say. That’s why the odds still favor Hong Kong’s peg to the US dollar remaining for the foreseeable future.

Follow William Pesek on Twitter at @WilliamPesek

HK dollar de-peg argument gains new currency

/cloudfront-us-east-2.images.arcpublishing.com/reuters/UPLTVMFE2VL7JKUXRSMGI6VQAA.jpg)

/cloudfront-us-east-2.images.arcpublishing.com/reuters/YILWC2LS7JMXTKAZ7CWAOIRECI.jpg)

/cloudfront-us-east-2.images.arcpublishing.com/reuters/RL6OTUSNHZOQ5BEBYF33YLSAMY.jpg)